The Makings of a Stock Trading Strategy - PART II¶

In PART I of The Makings of a Stock Trading Strategy, we had a look at equations describing trading strategy outcomes. At least, expressing their end results using an equal sign. Every equation used had a different insight into the nature of an evolving long-term trading portfolio from start to finish. This time we will add more equations that could greatly help your trading programs do better, and with ease, should you not already be doing it.

Doing a few automated short-term trades, here and there, is not enough to build a worthwhile long-term portfolio, there is always: where is the next trade? You need to feed your portfolio with a continuous series of trades. You might have years left to run to your long-term goal. Note that profits can also be had holding for long time intervals waiting for higher prices. This was also expressed in PART I, and it is not discouraged, on the contrary. It is only that the current emphasis will be on shorter-term trading. It is a world of its own.

We do want to deal with short-term trading, but nonetheless, to do so, we will need to look at the long-term math of the game. It sets boundaries and limits on what we can do within our self-imposed constraints, which can also be conditioned by market data, regulations, and trade availability. The finish line remains the main objective, and just getting there can be a tumultuous journey that still needs to unfold, a real roller-coaster ride.

Presently, I will look to solve the problem backward, from its endpoints. We know what the answer should be since it is measurable. It is our estimated endgame: $E[F(T)]$, a definite amount. However, it cannot be reached overnight, it will take years to reach that goal (see 20+years). The math used will try not only to set the goals but to also point out how it could be done. You have to determine how far do you want to go. That certainly is not my problem.

Nonetheless, we are left with finding ways to achieve that outcome. I will provide more equations to explain my point of view of the problem and let the underlying math, with its equal signs, support these expectations.

The chart in PART I showed that a multitude of trading strategies could provide the same overall result, and each strategy could be trading in a different manner based on different assumptions, using different stock selections and trading procedures.

It would be a matter of choosing which strategy suited you best since they all gave the same result. Often, we develop preferences based on what we know and the way we see or interpret the markets.

PART I said we could use trading methods we liked and achieve the same goal as many other methods used producing the same result. Whatever the trading methods, we know that the total generated profits will end up with $N \cdot \bar x$. Just two numbers with one being a counter. Those 2 numbers should get more attention. We also know that those two numbers could have totaled any other amounts if they were achievable.

Trading Methods¶

All trading methods part of the chart in PART I gave the same results: $F(t) = F_0 + N \cdot \bar x = 10,000,000.\,$ They all started with the same capital $F_0$ and managed the portfolio's trading from start to finish. This is not an article on finding the optimal trading strategy or the best Sharpe ratio, it is about finding a strategy that is feasible and acceptable to you. All combinations of $N \cdot \bar x$ gave the same answer. In the middle of all this, you are the mastermind. So take control.

The above equation could be replaced with $F(t) = F_0 \cdot (1 + g)^t$ since all strategies gave the same answer. Here the emphasis is now put on time $t$ and the portfolio's growth rate $g$. Thereby, showing that a portfolio can grow at an exponential rate. Time will prove itself an important, if not the most important element in a portfolio's quest for profits.

With the two equations, we have 5 interrelated variables: $F_0,\, N,\, \bar x,\, g,\,$ and $\,t\,$ to explain $F(t)$. The equations applied whatever the size of the starting capital $F_0$. We have the trade count which goes from $n = 1, \dots, N$. While $t$, well, you do not have a choice, time flies. $g$ and $\bar x$ are part of the end results, averages of the outcome of your trading strategy, and technically, mostly unknows at the start of the game.

It should be evident that if you want to trade short-term, you should seek trading methods that could generate a high number of trades ($N$) or a large average profit per trade ($\bar x$) or both at the same time, with for main constraint the size of your trading account.

A large $\bar x$ is available only if you give it time. And the more you will provide time, the fewer trades you will be able to do due to your capital constraints. Therefore, you will need to balance to some extent those two numbers to something that is suitable for your style of trading. And if what is presented below provides you with a better methodology, I hope you will put in the time to study it and absorb the mathematical backdrop implied in what will become this new vision of yours.

Whatever the outcome, the growth rate will be: $\,g = [\frac{F(T)}{F_0}]^{\frac{1}{t}} - 1.\,$ A direct result of your trading methods. $g$ is what you get after the fact, after having reached the finish line, or as you are getting close to it, near terminal time $T$. You can make estimates of $g$ as $N$ increases $E[g]_{N\uparrow} = \hat g \to g$. But these will only be guesstimates.

It is, however, much harder to really forecast $g$ over the next 20+ years: $F(t) = F_0 \cdot (1 + \hat g)^{20}$. Finacial academic literature has often proclaimed that the most expected average portfolio growth rate $\hat g$ tends to market averages over the long term: $\hat g \to r_m$. There is enough historical data to point to that effect.

However, you should want more by adding some alpha to your game which you will have to provide on your own: $\hat g = r_m + \alpha$. You want to outperform, not only your peers (who tend, on average, to $r_m$) but make sure you go beyond.

You know where you want to go, the direction is clear: $\to F(T)$, and you know how much you have to start with: $F_0.\,$ You have to determine for how long you want to do it and be ready to do it. It will take years. From $F(T)$, you can extract at what rate your portfolio needs to grow to achieve its goal. If you determine unrealistic or quasi-unreachable stuff, it won't be the market's fault, but your own for having utopian expectations. But that does not mean that you have to think small. Stay within what is achievable and possible, the endgame can be quite large and highly related to $F_0$. And note that $F_0$ is independent of market conditions, it is under your control.

How far can you go? It will all depend on your trading strategy design and its trade mechanics. I usually delegate the trading procedures to the underlying portfolio equations and trading logic. At least, they are there to guide the trading procedures.

An equal sign shows no mercy, no opinions, no emotions, no feelings. It only exists with: it is true or not?

The Randomness In Things¶

We will start by considering the game at hand as totally random as if stock prices went up or down based on a fair coin toss having a probability of $½$ and see how our trading strategy would behave. It is common knowledge that the market is not totally random or Gaussian, but also, for that matter, not entirely predictable either.

There are things to learn by looking at the game from the perspective of strict randomness, viewing it technically as a game of chance, somewhat akin to casino gambling, which is not that far from reality, especially in the case of short-term trading.

The total number of trades $N$ is composed of winning $W$ and losing $L$ trades. Total trades is simply their sum: $N = W + L$. In a fair coin toss trading contest, the expected number of trades for either side of the coin is: $E[W] = E[L] = \frac{N}{2}$. All you know about flipping a fair coin applies here. We will not dispute that. Nonetheless, the basics need to be restated so that later on there will be no confusion in the terminology used.

Let's make the game do 200 trades where we win or lose 200 on the flip of a coin. It gives us: $E_{200}[PFT] = 100 \cdot 200 + 100 \cdot (-200) = 0$, as the most expected outcome. You made 200 trades and have nothing to show for it.

There would be no real benefit in playing this game except for the entertainment. You could win, be lucky for sure, and end up positive (>0). However, it would not have been due to our flipping skills, but just plain luck of the draw.

We could also express this thing in terms of probabilities: $E_{200}[PFT] = F_0 + 200 \cdot 0.50^{W} + (-200) \cdot 0.50^{L} = F_0\;$ for $\,W = L = N/2$, which says the same thing.

If the stock market game was totally random, there would be no assured gain available since the expected value from one period to the next would be the previous value: $E[F(t+1)] = F(t)$. Thereby facing a martingale with a zero long-term expectancy. This would make the game not even worth playing, as was said, and a total waste of time.

You are in this for the money, so where is it?

Fixed Fraction¶

In my 2014 paper: Fixed Fraction, it was shown how you could control your trading portfolio using equations. Most of the paper dealt with fixed fractions as a portfolio control technique.

Fixed fraction is considering a trading strategy with an incremental betting system based on percentage moves. Here, it is not that you win or lose your bet, it is that you win or lose a fraction of your account. It is a major difference. First, the betting is related to the bet size, it will increase as the account grows and shrink as losses accumulate. This is not bad, you will be more daring on the way up, and more cautious in declines by reducing the size of your bets.

A series, or a sequence of trades could be expressed as: $$F(t) = F_0 \cdot (1 + f )^W \cdot (1 - f)^L$$ where again $\,N = W + L\,$ with $\,f\,$ the equal fraction for the profit target and stop loss. This equation has been around for a few centuries. Therefore, there is nothing new here, only recycling old stuff.

If a stock, after being bought, moves by either +$f\%$ or -$f\%$, it is sold, resulting in a corresponding profit or loss. This creates an equal boundary to trade execution. In fact, it creates 3 zones with boundaries: $p_i \cdot (1 + f\%)$ and $p_i \cdot (1 - f\%)$ with a no-trade zone in between where prices roam freely. A percent envelop indicator could provide this function and execute the trades when crossing the set boundaries. Even if prices were on a random-walk, they would be bound to hit these barriers here and there just due to the volatility and the randomness of things.

Since the intent is to deal with a large number of trades, we should expect this fraction to tend to some constant: $f \to \psi$. If your trading strategy sets a profit target at 10%, you should see $\psi \to 10\%$ over the long term as $N$ increases. It is not because you have not defined an explicit trade barrier that you are not using one. We are dealing with averages, and any method that operates with envelops (Donchian channels, Bollinger Bands, ATR breakouts, ...) will have their $f$ tend to $\psi$ on average. This means that this fixed fraction is more real than not, and appears in trading strategies more often than we might think.

For large $N$, in a random draw, we expect: $E[W] = E[L] \to \frac{N}{2}.\,$ And $F(t)$ will tend to zero following this design as $N$ increases: $$F(t)_{N \uparrow} = F_0 \cdot (1 + f)^W \cdot (1 - f)^L \to 0$$ The implication is that, simply due to randomness, the equal exit probability strategy will fail miserably since you will come to lose everything, including your initial capital. And depending on the value of $f$, and your hit rate, the process will be either slow or quite fast. But it will finish with zero nonetheless.

As the fixed equal fraction increases, it will accelerate the downfall. The more you trade, the more you are assured of losing it all. A real and total disaster in the making. Yet, we still see trading strategies using equal fixed fractions as trade exits. Some of those doing that are surprised to see their strategies fail or break down going forward. Go figure. It's what they programmed their strategy to do and it is doing it. It gets even worse when you see a fraction imbalance such as a profit target of +5$\%$ and stop loss of -10$\%$.

With $f = 0.20$, $N = 200$, and $W = N/2$ we get:

$F(t) = F_0 \cdot (1 + 0.20)^{100} \cdot (1 - 0.20)^{100} = 0.01687 \cdot F_0$. Reducing the original stake to 1.6% of its former value.

If you increase $N$ to 300 trades, it gets even worse:

$F(t) = F_0 \cdot (1 + 0.20)^{150} \cdot (1 - 0.20)^{150} = 0.00219 \cdot F_0$. This time, all that is left is 0.2% of the original capital.

The more $N$ increases, the more the portfolio decreases on its way to its final zero destination: $F(t) \to 0.$ In QuantConnect, the fixed fraction is given as "Average Win" and "Average Loss", both expressed as percentages. Here, in this article, I have made: $f = f_W = f_L$. While the distinction should be made, it was not necessary for this demonstration, and there was no loss of generality.

There is no reversing to the mean for this strategy, whatever anyone might claim, not even in a thousand years. Yet, the coin flip remained neutral, its expectancy remained $1/2$ on every single flip of the coin. It retained its long-term reversing to mean properties. So, based on the coin flip alone we should declare this strategy as a fair game. But, since the very structure of the game made us lose it all, could we even claim, on the other hand, that the game was fair? The equal sign is brutal.

This is only theoretical, you say. Well, not so much, think again. The above equations are expressed in terms of expectations and averages in a random-like environment. What is described is what is most probable of happening. Having $W < L$ would be even more detrimental and accelerate the downfall as well.

In a trading strategy where the profit target and the stop loss are set to the same value $f$, and where the trading system operates almost as if random, the above will definitely apply. It is almost a guarantee that the more you trade in this fashion, the more your trading account will shrink right down to zero if you let it.

As a consequence, one very basic and elementary piece of advice: do not trade that way, EVER.

Do not use equal trade triggering exits should your hit rate approach $1/2$. Note that some form of compensation could be had if the hit rate was higher, where $W > L$. But the higher hit rate will have to overcome the impact the fixed fraction will have on the system. There are better ways to deal with that.

Correcting The Long-Term Return Degradation¶

I often see trading strategies designed with equal profit targets and stop losses to then see the strategy designer wonder why his/her strategy is doing so poorly going forward as if it broke down. Their strategies were hopelessly flawed from the beginning and designed to fail simply due to their trading technique. It was not the market that put them under, it was themselves by not correcting this inherent compounding weakness.

Can this built-in return degradation be corrected? Yes, for sure, and, as a matter of fact, easily. It can even be reversed.

First, let's fix the decaying return problem, and then, add some needed alpha to the mix.

To start fixing return degradation, all that is required is to create a slight trade barrier imbalance:

$$(1 + f_W) \cdot (1 - f_L) > 1.0$$That's it. As simple as that.

Depending on the overall intentions, either of the following two equations will totally compensate for the return degradation: $$F(t) = F_0 \cdot (1 + \frac{f}{1 - f})^W \cdot (1 - f)^L$$ $$F(t) = F_0 \cdot (1 + f)^W \cdot (1 - \frac{f}{1 + f})^L$$ We can raise the profit target or reduced the stop loss. On an equal 10% profit target/stop loss scenario, we would have: $$E[F(t)] = F_0 \cdot (1 + 0.1111)^{W} \cdot (1 - 0.10)^{L} = F_0$$ $$E[F(t)] = F_0 \cdot (1 + 0.10)^{100} \cdot (1 - 0.0909)^{100} = F_0$$ As can be observed, these are two minor modifications. However, they do ensure the portfolio will not be destroyed. As an example, say we have a $\$$50 dollar stock with a 10$\%$ profit target/stop-loss setting, you would take profit at $\$$55 and the loss at $\$$45. Very ordinary stuff. And yet, if you do this as the general rule, it will destroy your portfolio.

However, if you change your exit settings, the profit target will be raised to $\$$55.55, or the stop loss will be set to $\$$45.45. Very minor requests in ever-fluctuating markets. And yet, it will be sufficient to stop future return degradation.

As can be observed, this does not make the strategy profitable. It generates absolutely no long-term profit, and for that matter, no loss either. It has an expected profit of zero: $E_{200}[PFT] \to 0$. That you do 200 trades or 1000, the outcome remains the same: $E_{1000}[PFT] \to 0$. At least, you are not losing all your capital. So, technically, problem solved.

Regardless, something better is needed. Losing all your money, or not making any, should not be considered desirable solutions.

Improving On The Design¶

Simply compensating on both sides would do it: $$E[F(t)] = F_0 \cdot (1 + 0.1111)^{100} \cdot (1 - 0.0909)^{100} = 2.73 \cdot F_0$$ making the strategy profit-generating. Yet, this was a modest request. You started with a 10% profit target and increased it to 11.11%. This cannot be considered a major strategy transformation. The same goes for moving the average stop loss from -10% to -9.0909%. Yet, these small changes made the strategy profitable over the long term.

We created this imbalance between the profit target and the stop loss. It compensated for the fact that after a 10% decline you need more than a 10% rise to return to the previous level since: $(1 + 0.10) \cdot (1 - 0.10) = 0.99$.

As you increase the number of trades, the above formula will also increase, for instance: $$E_{1000}[F(t)] = F_0 \cdot (1 + 0.1111)^{500} \cdot (1 - 0.0909)^{500} = 152.19 \cdot F_0$$ saying the strategy will not break down but continue to improve as the number of trades increases. Not because the market is doing something for you, but that you are doing something for yourself by creating this win-lose imbalance.

In fact, any positive imbalance can improve on the no-win scenario. And sufficiently compensating on both sides will make the strategy profit-generating: $(1 + 0.1111) \cdot (1 - 0.0909) = 1.01$.

It is our trade triggering logic that sets the general stop loss and profit target. It is a deliberate move on our part to set the profit target at 11.11% rather than at 10.00%, just like setting the stop loss at -9.0909%. Without even trading, we can determine the outcome of this trading policy in our randomly generated portfolio: $1.01^{100} = 2.73$. All this by forcing our strategy to respond to this 1% positive imbalance.

We can see a progression here. For not compensating, we had: $F(t) = F_0 \cdot (1 + f)^W \cdot (1 - f)^L \to 0$. Such that as $N$ increased, we lost it all.

Compensating for the return degration with either $F(t) = F_0 \cdot (1 + \frac{f}{1 - f})^W \cdot (1 - f)^L = F_0 \;$ or $\;F(t) = F_0 \cdot (1 + f)^W \cdot (1 - \frac{f}{1 + f})^L = F_0 \;$ we stopped losing capital. Making no money playing this game is certainly not enough.

With the double compensation, things really improved: $E_{200}[F(t)] = F_0 \cdot (1 + 0.1111)^{100} \cdot (1 - 0.0909)^{100} = 2.73 \cdot F_0$. There is profit generation.

This did not change the strategy's logic nor did it change the market, only our trading behavior settings and only by slightly increasing our expected average profit target and reducing the average stop loss. If you have a command that says: "set profit target = $f$", do make the adjustment to: "set profit target = $\frac{f}{1 + f}$". For the stop loss, likewise, adjust to $\frac{f}{1 - f}$. It will put you in positive profit territory, small, I admit, but nonetheless, positive, and in the right direction.

It does not end there, you can do much better.

Going For More¶

For one, I wanted more. So, I added a booster ($\,c\,$) as in: $$F(t) = F_0 \cdot (1 + \frac{f}{1 - (f + c)})^W \cdot (1- \frac{f}{1 + (f + c)})^L$$ This made the strategy more profitable and as a side effect also controllable. You could set the booster on/off whenever you wanted to, and at any level you felt comfortable with, all within your portfolio constraints. With a small booster such as: $c = 0.05$, and again $N = 200$, you got: $$F(t) = F_0 \cdot (1 + \frac{0.10}{1 - (0.10 + 0.05)})^W \cdot (1- \frac{0.10}{1 + (0.10 + 0.05)})^L = 7.57 \cdot F_0$$ With $c = 0.10$, we would get: $$F(t) = F_0 \cdot (1 + \frac{0.10}{1 - (0.10 + 0.10)})^W \cdot (1- \frac{0.10}{1 + (0.10 + 0.10)})^L = 21.69 \cdot F_0$$

Using the $\$$50.00 dollar stock example, and adding the 10$\%$ booster above, it would move the profit target to $\$$56.25 and the stop loss to $\$$45.83. Both, not considered big moves or unattainable. And yet, they would greatly improve on the overall performance.

If you wanted more bang for the buck: raising the profit target and keeping the booster at $c = 0.10$ would do it. $$F(t) = F_0 \cdot (1 + \frac{0.15}{1 - (0.15 + 0.10)})^W \cdot (1- \frac{0.15}{1 + (0.15 + 0.10)})^L = 232.48 \cdot F_0$$ You might want to raise the profit margin to some other level: $f +\Delta f = f + d$, as applied above: $$F(t) = F_0 \cdot (1 + \frac{f + d}{1 - (f + d + c)})^W \cdot (1- \frac{f + d}{1 + (f + d + c)})^L$$ You could also make these controllable functions if we wanted to: $$F(t) = F_0 \cdot (1 + \frac{f_t + d_t}{1 - (f_t + d_t + c_t)})^W \cdot (1- \frac{f_t + d_t}{1 + (f_t + d_t + c_t)})^L$$ thereby letting your trading procedures adjust the degree of trade agressiveness as you go along.

Care should be taken in choosing those profit targets and stop losses. Requesting too much can definitely surpass hyperbolas.

However, setting this trade barrier imbalance can easily be made. For instance, you could set arbitrary barriers such as a 15$\%$ profit target and a 8$\%$ stop loss: $(1 + 0.15) \cdot (1 - 0.92) = 1.058$, which would insure a positive outcome. And doing 200 randomly distributed trades would give: $F_0 \cdot 1.058^{100} = 280.91 \cdot F_0$.

This is all so simple.

The math only confirms that the barrier imbalance for the profit target and stop-loss is a way to go, even in a random trading environment. Not compensating for the return degradation is really a bad idea. So, going forward, over-compensate and do a little bit more to generate positive alpha. After all, it will be your trading account, not mine.

Make sure you put everything you can on your side so that the game goes your way. You have to plan for where you want to go. But whatever you want to do, you will not be able to escape the math of the game. Yet, you are still free to trade whichever way you want. Only remember, that it will be your way, therefore, take responsibility.

Of the potential trades your program might do, you might not remember the vast majority of those trades. But, the bottom line of your trading account will.

You can control and modulate $f, d, c,\,$ and $\,d$. And by your trading logic, also influence, if not control, $W$ and $L$ while pushing on $N$.

The Outcome¶

What does the outcome of these equations look like as $N$ increases? We are still in a random trading environment, and still dealing with averages and expectations. There are bell-shaped curves associated with these equations.

Even in this random-like artificial setting where $E[W] \to N/2$, meaning a strategy approaching a 50$\%$ hit rate, your trading strategy can make money simply by setting its profit target and stop-loss appropriately.

To be profitable, all that was required was to create this compensation imbalance barrier: $(1 + f_W)^W \cdot (1 - f_L)^L > 1.00$. It is remarkable, and yet, so simple. This says that even if your trading logic operated as if totally random you would be making money, and that you could control how much of it to a certain degree. The more the divergence, to a limit, between $f_W$ and $f_L$ the higher the expected profit, for example: $[(1 + 0.10)^W \cdot (1 - 0.05)^L]^{N/2} > 1.045^{N/2} = 1.045^{100} = 81.58$.

There are many ways that our strategies operate as if having fixed fractions for their exits. As was expressed above, all was put on the exit, not the entry. The exits had specific rules: reach the profit target or the stop loss at any time and the shares will be sold. Unless, along the way, you change your mind and got out anyway for whatever reason. There is always a tomorrow, except one.

We are the ones setting these parameters, not the program. These are directives that can be hardcoded. It is not the program that decides what the profit target will be. This makes a fixed fraction trading system your responsibility. You have to determine how your trade mechanics will operate. You are still involved in the trading logic and its monitoring. You are still responsible for the end results.

Imbalanced fixed fractions changed the game. From trying to find profitable trades in all the market's chaos, you will be sitting back waiting for the prices to come to you where trades will be executed on your terms at your boundary settings.

There is nothing predictive in the proposed game. You set your trading rules and you wait for stuff to happen. And since it will be boring, you will have your machine doing the work. This machine will effectively be your money printing machine, so protect it and do the same for your trading program.

All this could also be executed by hand and operated on Good-Til-Cancelled (GTC) orders. The orders would be, sell at profit target: $p_i \cdot (1 + \frac{f}{1 - (f + c)})$, or sell at the stop loss: $p_i \cdot (1 - \frac{f}{1 + (f + c)})$. A trade is closed, start the next one. And do this all the time.

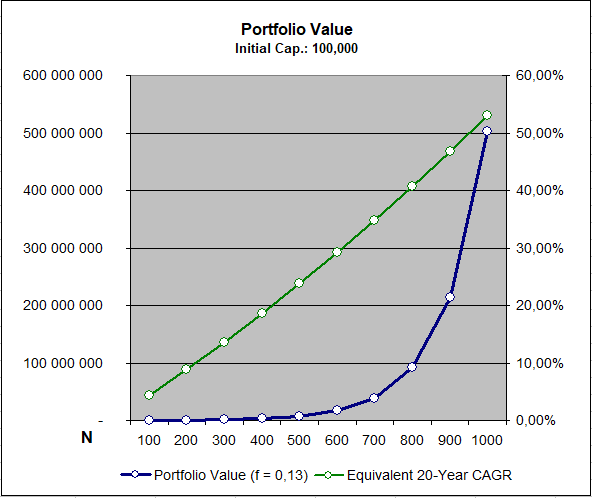

The following chart shows the double-compensated scenario where the fixed fraction $f$ was set to 13$\%$.

Fixed Fraction Chart ($f = 0.13$)

What is interesting in the above chart is the increasing CAGR as $N$ increases. The hit rate is still $1/2$, the expected outcome of a coin-tossing game. And yet, we have transformed a totally losing proposition into this money-making machine.

The CAGR of this compensated return strategy is increasing with $N$. The more you execute trades in the 20-year time period, the higher the expected CAGR.

A market-generated CAGR usually declines with time, it does not rise. Well, at least, in general, for most participants. And yet... you have this thing without even forecasting where it is going responding to its internal preset trade triggering mechanics. The more trades you can do under the improved compensated fraction settings, the better off you will be.

Here is the data that produced the above chart:

Fixed Fraction Table ($f = 0.13$)

The top part of the table generated the graph. We see $N$ gradually rising to 1000 and the winning trades set at $N/2$. Calculations are set on the last formula above with $d$ and $c$ set to zero.

The second part of the table shows the impact of adding a 2% booster to the mix. This cannot be considered a major change in one's portfolio perspective, but, nonetheless, it had a remarkable impact on the final outcome, all other things being equal. Just a nudge and the strategy produced 14.24 times more.

The last column shows the CAGR equivalent based on the formula presented earlier where the time interval for all cases (all values of $N$) was set to 20 years. The column gives the CAGR that would have been required over those 20 years to reach the displayed portfolio value.

What is outstanding in the above chart is the rising CAGR as the number of trades increases. Not only have we compensated for the return degradation, but we did put the system on an increasing CAGR as $N$ increases. All that was needed is a steady stream of trades distributed over those 20 years. You make more trades of this type and you make more.

The question now becomes, how many trades of this type can you execute over those 20 years based on the supplied compensating equations? How many 10$\%$ price moves are there in your tradable market universe? A simple answer: a lot.

How could you even improve on what was presented?

Improving The Odds¶

All the above examples were based on the expectation of a fair coin toss, a 50/50 proposition. But what if you had a slight edge? What if you could extract a higher hit rate, meaning: $W > L$? How would your trading strategy react then?

The US market has a slight long-term upward bias. This bias has been around for over two hundred years, and even without your intervention, can generate $W > L$ on its own. Your coin flips will tend to capture this underlying upside bias should you opt to use a fair coin. But, you might prefer using other methods to determine which stocks you will trade and how you will trade them.

With $f = 0.10$, $c = 0.10$, and $W = 100 + 5$ (a hit rate probability of $\;0.525$), we would have: $$F(t) = F_0 \cdot (1 + \frac{0.10}{1 - (0.10 + 0.10)})^{105} \cdot (1- \frac{0.10}{1 + (0.10 + 0.10)})^{95} = 60.40 \cdot F_0$$ Raising $f$ to $\,0.20$, would evidently raise the outcome: $$F(t) = F_0 \cdot (1 + \frac{0.20}{1 - (0.20 + 0.10)})^{105} \cdot (1- \frac{0.20}{1 + (0.20 + 0.10)})^{95} = 36,970.55 \cdot F_0$$ And with $f = 0.20$, and $\,W = 110,\,$ it would push the outcome even further out: $$F(t) = F_0 \cdot (1 + \frac{0.20}{1 - (0.20 + 0.10)})^{110} \cdot (1- \frac{0.20}{1 + (0.20 + 0.10)})^{90} = 299,455.01 \cdot F_0$$ Having $\,W = 110\,$ on 200 trades is the same as having a hit rate of 55%. It was not necessary to go to the moon, you only needed a little push.

As $N$ increases, we can see the impact a higher hit rate can have on a strategy. If we stay in the random-like trading environment, increasing $W$ becomes part of data variance, underlying upside bias, and luck. We should go for a more assured higher hit rate. To do so, we might have to abandon the random model and go for the real stuff.

That is where your own trading strategy comes in. You know how it behaves, what is its hit rate. It is given by your simulation software. The objective remains the same: $F(t) = F_0 + N \cdot \bar x,\,$ except this time it is your trading strategy that you want to improve upon. And there, you should go for more trades and a higher net average profit per trade: $F(t)^+ = F_0 + (N + \Delta n) \cdot (\bar x + \Delta \bar x).\,$ These incremental moves should improve the outcome of your trading strategy.

That we seek higher performance through a higher hit rate $W$ does not change the need for the return decay compensation. That still needs to be done anyway so that even if you end up with $W = N/2$ you will be ahead of the game. Increasing the hit rate is the domain of your trading strategy. How would you improve on your own hit rate? What would be required? How do you improve on $\bar x$? You could start with the market's long-term upward bias $W = 0.525 \cdot N$ which you could win even with the flip of a coin.

A better stock selection could help improve on $W$. Increasing $N$ over the same time interval would be another way to go.

This could be considered a total game-changer. Some have often wondered how I could make my trading strategies fly. Well, based on what was presented, it was relatively easy. I used compensating equations with boosters, amplifiers, and compounding as illustrated above with what it implied. Of note, it did take years to develop and refine.

This does not say: find or forecast trades that will generate a specific price target. It simply says: wait for the price to reach your price target, then execute. And do it again and again. It is proposing a sitting game. You should intend to wait for it and take the money.

If there is one thing to remember from all that was presented, it is compensate for the long-term return degradation which comes out of equal fixed fraction trading. It can be corrected and reversed so easily.

Now, based on the above, your task is to make it happen too. It is your choice. It has always been. Someone has already said: "No pain, no gain". Be wiser: "just take the gains, forget the pain".

© 2021, Guy Fleury