Aug. 30, 2019

When designing automated stock trading strategies, it is mainly to outperform other available methods of portfolio management, including other automated strategies. You can go to outperform over the short term, where you will find a lot of what should be considered market noise (unpredictability or volatility or randomness or whatever you want to call it). Or, go for the longer term, where the prevailing long-term market trend will be more visible.

Most of those trading strategies try to find corroborating evidence from past market data to extract some predictability from what could often simply be parts of this underlying long-term trend, the market's secular trend as can be seen in long-term market averages (for example, say, the SPY over a 30-year time span).

You can break down the underlying price movement into components or factors or profit sources or whatever you want to call them. But what you could find might be just some fractions of this underlying long-term market trend.

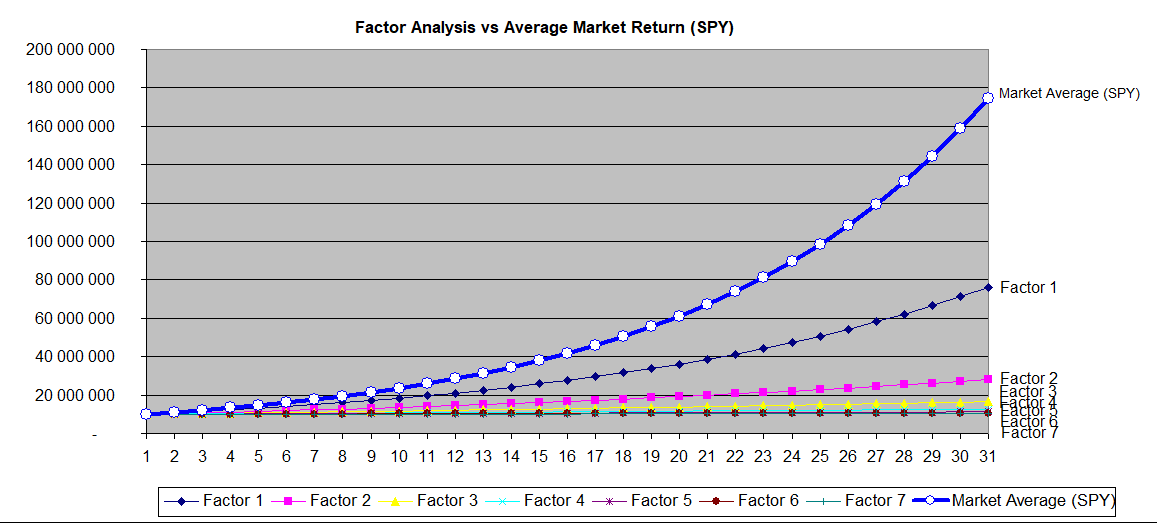

For instance, using principal component analysis, one could get the following chart where each factor contributes to the overall performance. However, when you add all the factors together, they might explain most of the variance, but they do not exceed the old standby: the market average benchmark.

(click to enlarge)

Therefore, what have you detected using those factors, if not just pieces of the underlying market trend? But, this market trend was available by doing no trading at all, just by buying the SPY. So, why go to all the trouble of trading so much to get less than doing nothing at all except initiating buying SPY and then sitting on your hands?

One should not consider those factors as alpha sources but merely as profit sources or components of the underlying secular trend where factor 1 explains the larger part of price variance, followed by factor 2, and so on. It is like looking at the Fama-French factors, which lead to the efficient market portfolio residing on the efficient frontier, which turns out to be the actual market average, which again could be expressed in some benchmark like SPY.

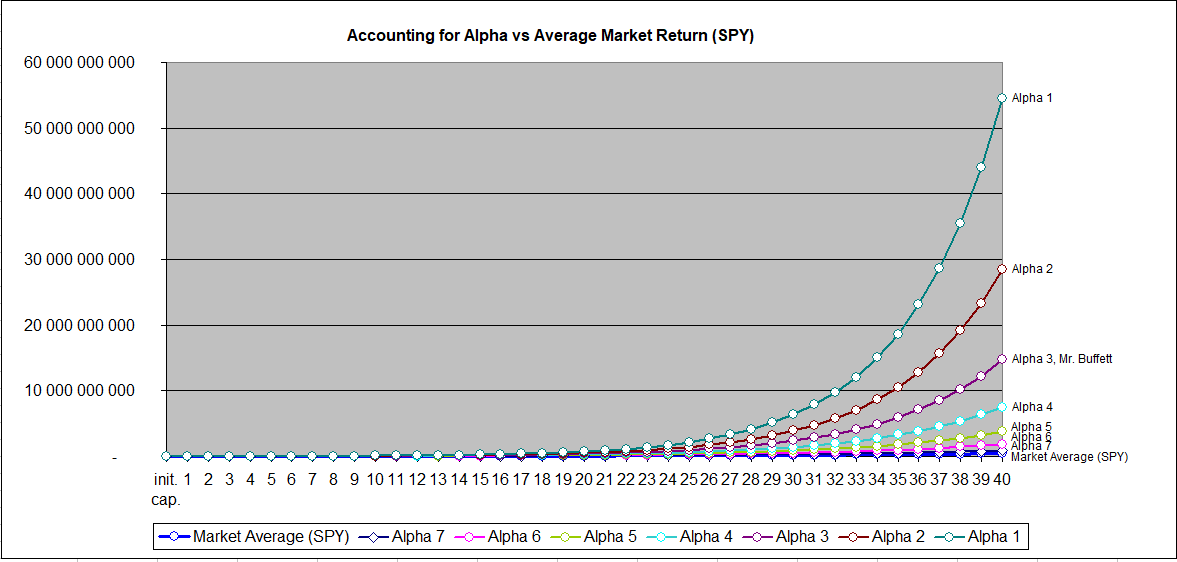

To exceed market average performance, you need some real alpha which should be measured as the excess over and above the market average. The following chart expresses this point:

(click to enlarge)

The above chart shows alpha factors by order of desirability (the higher, the better, evidently). For example, alpha 3 represents a 20% CAGR over the 30-year period. It also corresponds to Mr. Buffett's average long-term CAGR. Alpha 2 is 2% higher (22%), and alpha 1 is 4% higher (24%). Alpha 1 and alpha 2 show how much of a difference those added 2% can make in the overall scheme of things. They are more desirable but also much harder to obtain.

To get there, you will have to do more than just sit on your hands. You will have to be actively trading or have better predictive tools than your peers. Because this is a compounding return game, giving more time or getting a higher alpha factor above alpha 1 will push overall performance even higher.

But time also gets to be a major player in this game. Keep everything the same and just add 10 more years to the above scenarios. The first graph (the factor chart above) would now look like the following, where the time horizon has been increased to 40 years:

(click to enlarge)

The picture did not get any better. In fact, the sum of the factors still did not reach the expected average market return. A return that could be achieved by doing absolutely nothing other than sitting tight and waiting. The spread between the average market return (SPY) and the best of the factors (factor 1) is increasing. The same with all the other factors showing that even with positive results their sum is much less than the average benchmark. In fact, the total for all 7 factors is only 56.5% of what SPY could have paid off while doing no work at all.

So, when you see some factor analysis of some kind, what is it that they are grabbing? Is it part of this secular trend which is like given away for free, or is it just the remnants of this secular trend? Are they not, nonetheless, underperforming the available averages?

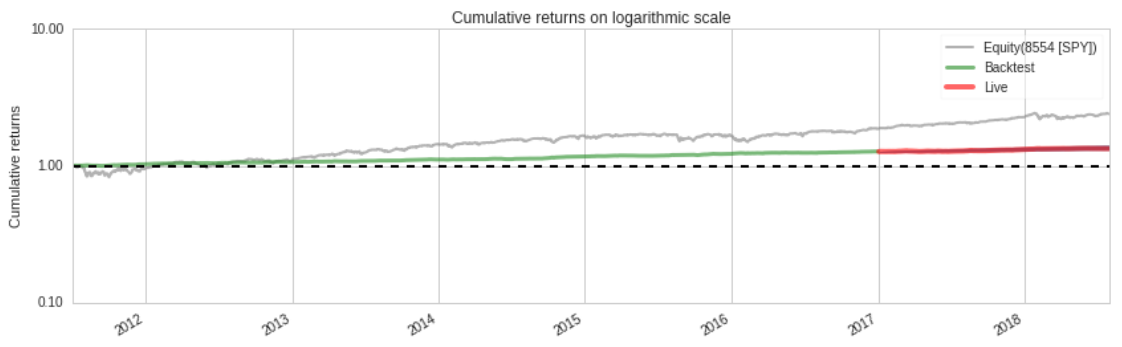

In a Quantopian simulation, this type of chart is often seen where all factors are combined into a single one resulting in the following look:

(click to enlarge)

There is nothing wrong with such a chart as long as it is what you were looking for, subject to whatever constraints you wanted your portfolio to adhere to. However, it should be noted that those constraints come at a cost. And it is the difference between the market averages and the sum of the factors as illustrated in the above chart. The final result remains, it is a trading strategy that is underperforming its benchmark.

However, what I think is more “important” is adding time to the alpha scenario. It is where we see the power of compounding. For instance, alpha 1 is 120.5 times larger than the market average (SPY). And yet, it is only at a 24% compounding rate of return. 4 alpha points above Mr. Buffett's long-term CAGR. Imagine if your alpha 1 was at an even higher setting.

(click to enlarge)

As a basic tenant to any automated stock trading strategy, the main objective should always be to outperform the market averages no matter what or how you want to do it. Otherwise, you need pretty compelling reasons to adopt the factor analysis counterpart where even if your objective is having low volatility you might find that the opportunity cost of that particular objective can be quite high. Simply compare the alpha 1 in the last chart to the sum of all factors in the 40-year factor chart. One can execute either chart.

I think that all the effort in designing automated trading strategies should be concentrated on extracting the highest alpha you possibly can over the longest time interval. And this can be done by looking at the problem from an alpha perspective and not necessarily from a profit-factor perspective.

It is always a matter of choice. We remain the designers of our own automated trading strategies.

Aug. 30, 2019, © Guy R. Fleury. All rights reserved.